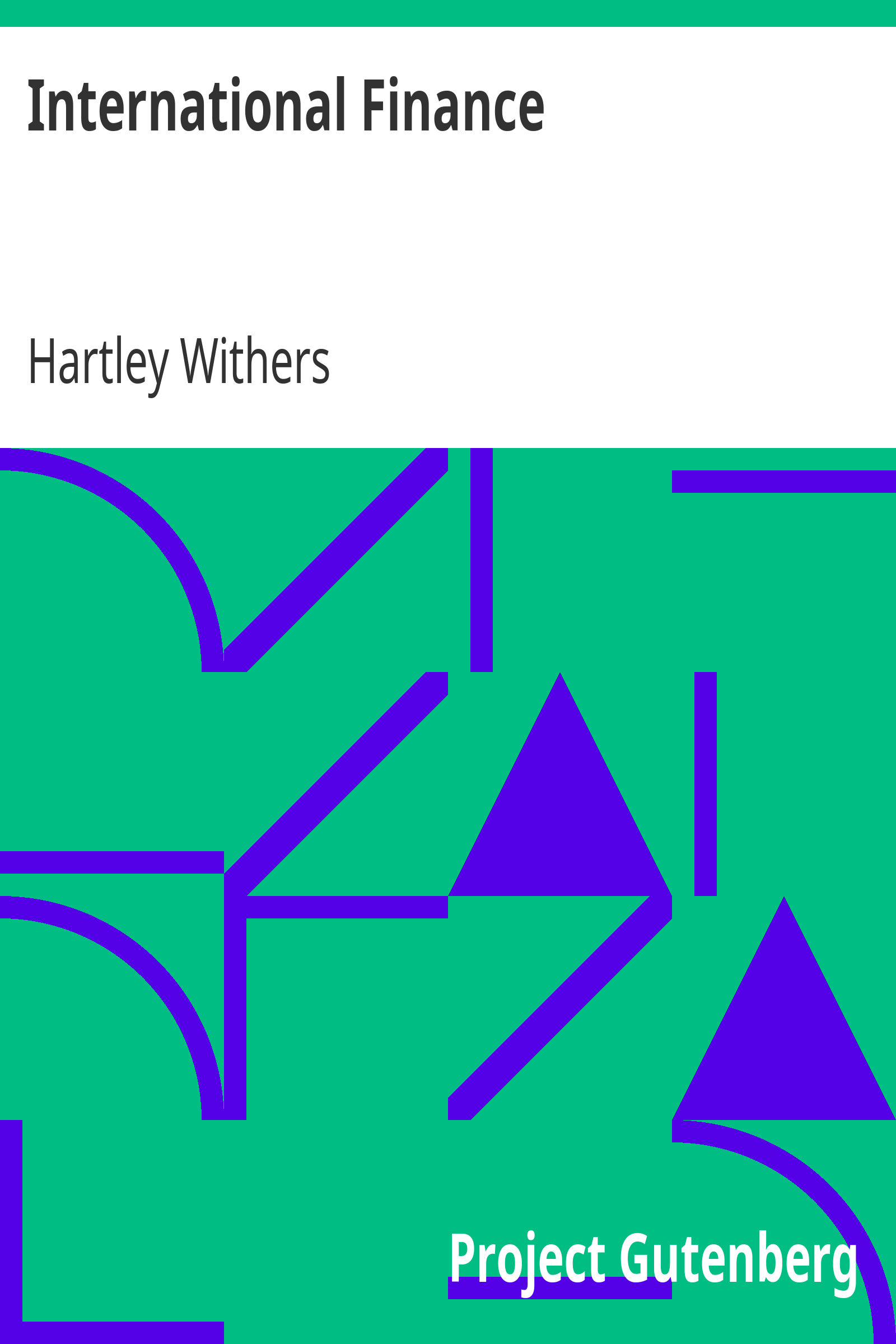

Notes Issued £56,908,235 Government Debt £11,015,100

Other Securities 7,434,900

Gold Coin and Bullion 38,458,235

Silver Bullion ---

----------- -----------

£56,908,235 £56,908,235

----------- -----------

BANKING DEPARTMENT.

Proprietors' Capital £14,553,000 Government Securities £11,005,126

Rest 3,431,484 Other Securities 33,623,288

Public Deposits 13,318,714 Notes 27,592,980

Other Deposits 42,485,605 Gold and Silver Coin 1,596,419

Seven Day and other

Bills 29,010

----------- -----------

£73,817,813 £73,817,813

----------- -----------

With the Bank of England thus acting as a centre to the system, there has grown up around it a circle of the great joint stock banks, which provide credit and currency for commerce and finance by lending money and taking it on deposit, or on current account. These banks work under practically no legal restrictions of any kind with regard to the amount of cash that they hold, or the use that they make of the money that is entrusted to their keeping. They are not allowed, if they have an office in London, to issue notes at all, but in all other respects they are left free to conduct their business along the lines that experience has shown them to be most profitable to themselves, and most convenient for their customers. Being joint stock companies they have to publish periodically, for the information of their shareholders, a balance sheet showing their position. Before the war most of them published a monthly statement of their position, but this habit has lately been given up. No legal regulations guide them in the form or extent of the information that they give in their balance sheets, and their great success and solidity is a triumph of unfettered business freedom. This absence of restriction gives great elasticity and adaptability to the credit machinery of London. Here is a specimen of one of their balance sheets, slightly simplified, and dating from the days before the war:—

Capital (subscribed) £14,000,000

----------

Paid up 3,500,000

Reserve 4,000,000

Deposits 87,000,000

Circular Notes, etc. 3,000,000

Acceptances 6,000,000

Profit and loss 500,000

-----------

£104,000,000

-----------

ASSETS

Cash in hand and

at Bank of England £12,500,000

Cash at call and

short notice 13,000,000

Bills discounted 19,000,000

Govt. Securities 5,000,000

Other Investments 4,500,000

Advances and loans 42,000,000

Liability of customers

on account of

Acceptances 6,000,000

Promises 2,000,000

-----------

£104,000,000

-----------

On one side are the sums that the bank has received, in the shape of capital subscribed, from its shareholders, and in the shape of deposits from its customers, including Dr. Pillman and thousands like him; on the other the cash that it holds, in coin, notes and credit at the Bank of England, its cash lent at call or short notice to bill brokers (of whom more anon) and the Stock Exchange, the bills of exchange that it holds, its investments in British Government and other stocks, and the big item of loans and advances, through which it finances industry and commerce at home. It should be noted that the entry on the left side of the balance sheet, "Acceptances," refers to bills of exchange which the bank has accepted for merchants and manufacturers who are importing goods and raw material, and have instructed the foreign exporters to draw bills on their bankers. As these merchants and manufacturers are responsible to the bank for meeting the bills when they fall due, the acceptance item is balanced by an exactly equivalent entry on the other side, showing this liability of customers as an asset in the bank's favour.

This business of acceptance is done not only by the great banks, but also by a number of private firms with connections in foreign countries, and at home, through which they place their names and credit at the disposal of people less eminent for wealth and position, who pay them a commission for the use of them.

Other wheels in London's credit machinery are the London offices of colonial and foreign banks, and the bill brokers or discount houses which deal in bills of exchange and constitute the discount market. Thus we see that there is in London a highly specialized and elaborate machinery for making and dealing in these bills, which are the currency of international trade. Let us recapitulate the history of the bill and see the part contributed to its career by each wheel in the machine. We imagined a bill drawn by an Argentine seller against a cargo of wheat shipped to an English merchant. The bill will be drawn on a London accepting house, to whom the English merchant is liable for its due payment. The Argentine merchant, having drawn the bill, sells it to the Buenos Ayres branch of a South American bank, formed with English capital, and having its head office in London. It is shipped to London, to the head office of the South American bank, which presents it for acceptance to the accepting house on which it is drawn, and then sells it to a bill broker at the market rate of discount. If the bill is due three months after sight, and is for £2000, and the market rate of discount is 4 per cent. for three months' bills, the present value of the bill is obviously £1980. The bill broker, either at once or later, probably sells the bill to a bank, which holds it as an investment until its due date, by which time the importer having sold the wheat at a profit, pays the money required to meet the bill to his banker and the transaction is closed. Thus by means of the bill the exporter has received immediate payment for his wheat, the importing merchant has been supplied with credit for three months in which to bring home his profit, and the bank which bought the bill has provided itself with an investment such as bankers love, because it has to be met within a short period by a house of first-rate standing.

All this elaborate, but easily working machinery has grown up for the service of commerce. It is true that bills of exchange are often drawn by moneylenders abroad on moneylenders in England merely in order to raise credit, that is to say, to borrow money by means of the London discount market. Sometimes these credits are used for merely speculative purposes, but in the great majority of cases they are wanted for the furtherance of production in the borrowing country. The justification of the English accepting houses, and bill brokers, and banks (in so far as they engage in this business), is the fact that they are assisting trade, and could not live without trade, and that trade if deprived of their services would be gravely inconvenienced and could only resume its present activity by making a new machinery more or less on the same lines. The bill whose imaginary history has been traced, came into being because the drawer had a claim on England through a trade transaction. He was able to sell it to the South American bank only because the bank knew that many other people in Argentina would have to make payments to England and would come to it and ask it for drafts on London, which, by remitting this bill to be sold in London, it would be able to supply. International finance is so often regarded as a machinery by which paper wealth is manufactured out of nothing, that it is very important to remember that all this paper wealth only acquires value by being ultimately based on something that is grown or made and wanted to keep people alive or comfortable, or at least happy in the belief that they have got something that they thought they wanted, or which habit or convention obliged them to possess.

FOOTNOTES:

All this imaginary picture is of events before the war. At present Dr. Pillman, being a patriotic citizen, is saving much faster than before, and putting every pound that he can save into the hands of the British Government by subscribing to War Loans and buying Exchequer bonds. He is too old to go and do medical work at the front, so he does the next best thing by cutting down his expenses and finding money for the war.

CHAPTER III

So far we have only considered what happens to the money of those who save as long as it is left in the hands of their bankers, and we have seen that it is only likely to be employed internationally, if invested by bankers in bills of exchange which form a comparatively small part of their assets. It is true that bankers also invest money in securities, and that some of these are foreign, but here again the proportion invested abroad is so small that we may be reasonably sure that any money left by us in the hands of our bankers will be employed at home.

But in actual practice those who save do not pile up a large balance at their banks. They keep what is called a current account, consisting of amounts paid in in cash or in cheques on other banks or their own bank, and against this account they draw what is needed for their weekly and monthly payments; sometimes, also, they keep a certain amount on deposit account, that is an account on which they can only draw after giving a week's notice or more. On their deposit account they receive interest, on their current account they may in some parts of the country receive interest on the average balance kept. But the deposit account is most often kept by people who have to have a reserve of cash quickly available for business purposes. The ordinary private investor, when he has got a balance at his bank big enough to make him feel comfortable about being able to meet all probable outgoings, puts any money that he may have to spare into some security dealt in on the Stock Exchange, and so securities and the Stock Exchange have to be described and examined next. They are very much to the point, because it is through them that international finance has done most of its work.

Securities, then, are the stocks, shares and bonds which are given to those who put money into companies, or into loans issued by Governments, municipalities and other public bodies. Let us take the Governments and public bodies first, because the securities issued by them are in some ways simpler than those created by companies.

When a Government wants to borrow, it does so because it needs money. The purpose for which it needs it may be to build a railway or canal, or make a harbour, or carry out a land improvement or irrigation scheme, or otherwise work some enterprise by which the power of the country to grow and make things may be increased. Enterprises of this kind are usually called reproductive, and in many cases the actual return from them in cash more than suffices to meet the interest on the debt raised to carry them out, to say nothing of the direct benefit to the country in increasing its output of wealth. In England the Government has practically no debt that is represented by reproductive assets. Our Government has left the development of the country's resources to private enterprise, and the only assets from which it derives a revenue are the Post Office buildings, the Crown lands and some shares in the Suez Canal which were bought for a political purpose. Governments also borrow money because their revenue from taxes is less than the sums that they are spending. This happens most often and most markedly when they are carrying on war, or when nations are engaged in a competition in armaments, building navies or raising armies against one another so as to be ready for war if it happens. This kind of debt is called dead-weight debt, because there is no direct or indirect increase, in consequence of it, in the country's power to produce things that are wanted. This kind of borrowing is generally excused on the ground that provision for the national safety is a matter which concerns posterity quite as much as the present generation, and that it is, therefore, fair to leave posterity to pay part of the bill.

Municipalities likewise borrow both for reproductive purposes and for objects from which no direct revenue can be expected. They may invest money lent them in gas or electric works or water supply or tramways, and get an income from them which will more than pay the interest on the money borrowed. Or they may put it into public parks and recreation grounds or municipal buildings, or improvements in sanitation, thereby beautifying and cleansing the town. If they do these things in such a way as to make the town a pleasanter and healthier place to live in, they may indirectly increase their revenue; but if they do them extravagantly and badly, they run the risk of putting a burden on the ratepayers that will make people shy of living within their borders.

Whatever be the object for which the loan is issued, the procedure is the same by which the money is raised. The Government or municipality invites subscriptions through a bank or through some great financial house, which publishes what is called a prospectus by circular, and in the papers, giving the terms and details of the loan. People who have money to spare, or are able to borrow money from their bankers, and are attracted by the terms of the loan, sign an application form which is issued with the prospectus, and send a cheque for the sum, usually 5 per cent. of the amount that they apply for, which is payable on application. If the loan is over-subscribed, the applicants will only receive part of the sums for which they apply. If it is not fully subscribed, they will get all that they have asked for, and the balance left over will be taken up in most cases by a syndicate formed by the bank or firm that issued the loan, to "underwrite" it. Underwriting means guaranteeing the success of a loan, and those who do so receive a commission of anything from 1 to 3 per cent.; if the loan is popular and goes well the underwriters take their commission and are quit; if the loan is what the City genially describes as a "frost," the underwriters may find themselves saddled with the greater part of it, and will have the pleasure of nursing it until such time as the investing public will take it off their hands. Underwriting is thus a profitable business when times are good, and the public is feeding freely, but it can only be indulged in by folk with plenty of capital or credit, and so able to carry large blocks of stock if they find themselves left with them.

To take a practical example, let us suppose that the King of Ruritania is informed by his Minister of Marine that a battleship must at once be added to its fleet because his next door neighbour is thought to be thinking of making himself stronger on the water, while his Minister of Finance protests that it is impossible, without the risk of serious trouble, to add anything further to the burdens of the taxpayers. A loan is the easy and obvious way out. London and Paris between them will find two or three millions with pleasure. That will be enough for a battleship and something over in the way of new artillery for the army which can be ordered in France so as to secure the consent of the French Government, which was wont to insist that a certain proportion of any loan raised in Paris must be spent in the country. (It need hardly be said that all these events are supposed to be happening in the years before the war.) Negotiations are entered into with a group of French banks and an English issuing house. The French banks take over their share, and sell it to their customers who are, or were, in the habit of following the lead of their bankers in investment with a blind confidence, that gave the French banks enormous power in the international money market. The English issuing house sends round a stockbroker to underwrite the loan. If the issuing house is one that is usually successful in its issues, the privilege of underwriting anything that it brings out is eagerly sought for. Banks, financial firms, insurance companies, trust companies and stockbrokers with big investment connections will take as much underwriting as they are offered, in many cases without making very searching inquiry into the terms of the security offered. The name of the issuing house and the amount of the underwriting commission —which we will suppose in this case to be 2 per cent.—is enough for them. They know that if they refuse any chance of underwriting that is offered, they are not likely to get a chance when the next loan comes out, and since underwriting is a profitable business for those who can afford to run its risks, many firms put their names down for anything that is put before them, as long as they have confidence in the firm that is handling the loan. This power in the hands of the big issuing houses, to get any loan that they choose to father underwritten in a few hours by a crowd of eager followers, gives them, of course, enormous strength and lays a heavy responsibility on them. They only preserve it by being careful in the use of it, and exercising great discrimination in the class of securities that they handle.

While the underwriting is going on the prospectus is being prepared by which the subscriptions of the public are invited, and in the meantime it will probably happen that the newspapers have had a hint that a Ruritanian loan is on the anvil, so that preliminary paragraphs may prepare an atmosphere of expectancy. News of a forthcoming new issue is always a welcome item in the dull routine of a City article, and the journalists are only serving their public and their papers in being eager to chronicle it. Lurid stories are still handed down by City tradition of how great City journalists acquired fortunes in days gone by, by being allotted blocks of new loans so that they might expand on their merits and then sell them at a big profit when they had created a public demand for them. There seems to be no doubt that this kind of thing used to happen in the dark ages when finance and City journalism did a good deal of dirty business between them. Now, the City columns of the great daily papers have for a very long time been free from any taint of this kind, and on the whole it may be said that finance is a very much cleaner affair than either law or politics. It is true that swindles still happen in the City, but their number is trivial compared with the volume of the public's money that is handled and invested. It is only in the by-ways of finance and in the gutters of City journalism that the traps are laid for the greedy and gullible public, and if the public walks in, it has itself to blame. A genuine investor who wants security and a safe return on his money can always get it. Unfortunately the investor is almost always at the same time a speculator, and is apt to forget the distinction; and those who ask for a high rate of interest, absolute safety and a big rise in the prices of securities that they buy are only inviting disaster by the greed that wants the unattainable and the gullibility that deludes them into thinking they can have it.

To return to our Ruritanian loan, which we left being underwritten. The prospectus duly comes out and is advertised in the papers and sown broadcast over the country through the post. It offers £1,500,000 (part of £3,000,000 of which half is reserved for issue in Paris), 4-1/2 per cent. bonds of the Kingdom of Ruritania, with interest payable on April 1st and October 1st, redeemable by a cumulative Sinking Fund of 1 per cent., operating by annual drawings at par, the price of issue being 97, payable as to 5 per cent. on application, 15 per cent. on allotment and the balance in instalments extending over four months. Coupons and drawn bonds are payable in sterling at the countinghouse of the issuing firm. The extent of the other information given varies considerably. Some firms rely so far on their own prestige and the credit of those on whose account they offer loans, that they state little more than the bare terms of the issue as given above. Others deign to give details concerning the financial position of the borrowing Government, such as its revenue and expenditure for a term of years, the amount of its outstanding debt, and of its assets if any. If the credit of the Kingdom of Ruritania is good, such a loan as here described would be, or would have been before the war, an attractive issue, since the investor would get a good rate of interest for his money, and would be certain of getting par or £100, some day, for each bond for which he now pays £97. This is ensured by the action of the Sinking Fund of 1 per cent. cumulative, which works as follows. Each year, as long as the loan is outstanding the Kingdom of Ruritania will have to put £165,000 in the hands of the issuing houses, to be applied to interest and Sinking Fund. In the first year interest at 4-1/2 per cent. will take £135,000 and Sinking Fund (1 per cent. of £3,000,000) £30,000; this £30,000 will be applied to the redemption of bonds to that value, which are drawn by lot; so that next year the interest charge will be less and the amount available for Sinking Fund will be greater; and each year the comfortable effect of this process continues, until at last the whole loan is redeemed and every investor will have got his money back and something over. The effect of this obligation to redeem, of course, makes the market in the loan very steady, because the chance of being drawn at par in any year, and the certainty of being drawn if the investor holds it long enough, ensures that the market price will be strengthened by this consideration.

Such being the terms of the loan we may be justified in supposing—if Ruritania has a clean record in its treatment of its creditors, and if the issuing firm is one that can be relied on to do all that can be done to safeguard their interests, that the loan is a complete success and is fully subscribed for by the public. The underwriters will consequently be relieved of all liability and will pocket their 2 per cent., which they have earned by guaranteeing the success of the issue. If some financial or political shock had occurred which made investors reluctant to put money into anything at the time when the prospectus appeared or suggested the likelihood that Ruritania might be involved in war, then the underwriters would have had to take up the greater part of the loan and pay for it out of their own pockets; and this is the risk for which they are given their commission. Ruritania will have got its money less the cost of underwriting, advertising, commissions, 1 per cent. stamp payable to the British Government, and the profit of the issuing firm. Some shipyard in the north will lay down a battleship and English shareholders and workmen will benefit by the contract, and the investors will have got well secured bonds paying them a good rate of interest and likely to be easily saleable in the market if the holders want to turn them into cash. The bonds will be large pieces of paper stating that they are 4-1/2 per cent, bonds of the Kingdom of Ruritania for £20, £100, £500 or £1000 as the case may be, and they will each have a sheet of coupons attached, that is, small pieces to be cut off and presented at the date of each interest payment; each one states the amount due each half year and the date when it will have to be met.

Bonds are called bearer securities, that is to say, possession of them entitles the bearer to receive payment of them when drawn and to collect the coupons at their several dates. They are the usual form for the debts of foreign Governments and municipalities, and of foreign railway and industrial companies.

In England we chiefly affect what are called registered and inscribed stocks—that is, if our Government or one of our municipalities issues a loan, the subscribers have their names registered in a book by the debtor, or its banker, and merely hold a certificate which is a receipt, but the possession of which is not in itself evidence of ownership. There are no coupons, and the half-yearly interest is posted to stockholders, or to their bankers or to any one else to whom they may direct it to be sent. Consequently when the holder sells it is not enough for him to hand over his certificate, as is the case with a bearer security, but the stock has to be transferred into the name of the buyer in the register kept by the debtor, or by the bank which manages the business for it.

When the securities offered are not loans by public bodies, but represent an interest in a company formed to build a railway or carry on any industrial or agricultural or mining enterprise, the procedure will be on the same lines, except that the whole affair will be on a less exalted plane. Such an issue would not, save in exceptional circumstances, as when a great railway is offering bonds or debenture stock, be fathered by one of the leading financial firms. Industrial ventures are associated with so many risks that they are usually left to the smaller fry, and those who underwrite them expect higher rates of commission, while subscribers can only be tempted by anticipations of more mouth-filling rates of interest or profit. This distinction between interest and profit brings us to a further difference between the securities of companies and public bodies. Public bodies do not offer profit, but interest, and the distinction is very important. A Government asks for your money and promises to pay a rate for it, whether the object on which the money is spent be profit-earning or no, and, if it is, whether a profit be earned or no. A company asks subscribers to buy it up and become owners of it, taking its profits, that it expects to earn, and getting no return at all on their money if its business is unfortunate and the profits never make their appearance. Consequently the shareholders in a company run all the risks that industrial enterprise is heir to, and the return, if any, that comes into their pockets depends on the ability of the enterprise to earn profits over and above all that it has to pay for raw material, wages and other working expenses, all of which have to be met before the shareholder gets a penny.

In order to meet the objections of steady-going investors to the risks involved by thus becoming industrial adventurers, a system has grown up by which the capital of companies is subdivided into securities that rank ahead of one another. Companies issue debts, like public bodies, in the shape of bonds or debenture stocks, which entitle the holders of them to a stated rate of interest, and no more, and are often repayable at a due date, by drawings or otherwise. These are the first charge on the concern after wages and other working expenses have been paid, and the shareholders do not get any profit until the interest on the company's debt has been met. Further, the actual capital held by the shareholders is generally divided into two classes, preference and ordinary, of which the preference take a fixed rate before the ordinary shareholders get anything, and the ordinary shareholders take the whole of any balance left over. Sometimes, the preference holders have a right to further participation after the ordinary have received a certain amount of dividend, or share of profit, and there are almost endless variations of the manner in which the different classes of holders may claim to divide the profits, by means of preference, preferred, ordinary, preferred ordinary, deferred ordinary, founders' shares, management shares, etc., etc.

All these variations in the position of the shareholder, however, do not alter the great essential difference between him and the creditor, the man who lends money to a Government or enterprise with a fixed rate of interest, and, in most cases, a claim for repayment sooner or later. The shareholder, whether preference or ordinary, puts his money into a venture with no claim for repayment, unless the company is wound up, in which case his claim ranks, of course, after that of every creditor. If he wants to get his money out again he can only do so by selling his stock or shares at any price that they will fetch in the stock market.

Thus, if we take as an example a Brewery company with a total debt and capital of three millions, we may suppose that it will have a million 4-1/2 per cent, debenture stock, entitling the creditors who own it to interest at that rate, and repayment in 1935, a million of 6 per cent. cumulative preference stock, giving holders a fixed dividend, if earned, of 6 per cent, which dividend and all arrears have to be paid before the ordinary shareholders get anything, and a million in ordinary shares of £10 each, whose holders take any balance that may be left. This is the total of the money that has been received from the public when the company was floated and put into the brewery plant, tied houses, or other assets out of which the company makes its revenue.

These bonds and stocks and shares are the machinery of international finance, by which moneylenders of one nation provide borrowers in others with the wherewithal to carry out enterprises, or make payments for which they have not cash available at home. It was shown in a previous chapter that bills of exchange are a means by which the movements of commodities from market to market are financed, and the gap in time is bridged between production and consumption. Stock Exchange securities are more permanent investments, put into industry for longer periods or for all time. Midway between them are securities such as Treasury bills with which Governments raise the wind for a time, pending the collection of revenue, and the one or two years' notes with which American railroads lately financed themselves for short periods, in the hope that the conditions for an issue of bonds with longer periods to run, might become more favourable.

So far we have only considered the machinery by which these securities are created and issued to the public, but it must not be supposed that investment is only possible when new securities are being offered. Many investors have a prejudice against ever buying a new security, preferring those which have a record and a history behind them, and buying them in the market whenever they have money to invest. This market is the Stock Exchange in which securities of all kinds and of all countries are dealt in. Following the history of the Ruritanian loan, we may suppose that it will be dealt in regularly in that section of the Stock Exchange in which the loans of Foreign Governments are marketed. Any original subscriber who wants to turn his bonds into money can do so by instructing his broker to sell them; anyone who wants to do so can acquire a holding in them by a purchase. The terms on which they will be bought or sold will depend on the variations in the demand for, and supply of, them. If a number of holders want to sell, either because they want cash for other purposes, or because they are nervous about the political outlook, or because they think that money is going to be scarce and so there will be better opportunities for investment later on, then the price will droop. But if the political sky is serene and people are saving money fast and investing it in Stock Exchange securities, then the price will go up and those who want to buy it will pay more. The price of all securities, as of everything else, depends on the extent to which people who have not got them demand them, in relation to the extent to which those who have got them are ready to part with them. Price is ultimately a question of what people think about things, and this is why the fluctuations in the price of Stock Exchange securities are so incalculable and often so irrational. If a sufficient number of misguided people with money in their pockets think that a bad security is worth buying they will put the price of it up in the face of the logic of facts and all the arguments of reason. These wild fluctuations, of course, take place chiefly in the more speculative securities. Shares in a gold mine can go to any price that the credulity of buyers dictates, since there is no limit to the amount of gold that people can imagine to be under the ground in its territory.

All the Stock Exchanges of the world are in communication with one another by telegraph, or telephone, and so their feelings about prices react on one another's nerves and imaginations, and the Stock Exchange price list may be said to be the language of international finance, as the bill of exchange is its currency.

CHAPTER IV

We have seen that finance becomes international when capital goes abroad, by being lent by investors in one country to borrowers in another, or by being invested in enterprises formed to carry on some kind of business abroad. We have next to consider why capital goes abroad and whether it is a good or a bad thing, for it to do so.

Capital goes abroad because it is more wanted in other countries than in the country of its origin, and consequently those who invest abroad are able to do so to greater advantage. In countries like England and France, where there have been for many centuries thrifty folk who have saved part of their income, and placed their savings at the disposal of industry, it is clear that industry is likely to be better supplied with capital than in the new countries which have been more lately peopled, and in which the store of accumulated goods is less adequate to the industrial needs of the community. For we must always remember that though we usually speak and think of capital as so much money it is really goods and property. In England money consists chiefly of credit in the books of banks, which can only be created because there is property on which the banks can make advances, or because there is property expressed in securities in which the banks can invest or against which they can lend. Because our forefathers did not spend all their incomes on their own personal comfort and amusement but put a large part of them into railways and factories, and shipbuilding yards, our country is now reasonably well supplied with the machinery of production and the means of transport. Whether it might not be much better so equipped is a question with which we are not at present concerned. At least it may be said that it is more fully provided in these respects than new countries like our colonies, America and Argentina, or old countries like Russia and China in which industrial development is a comparatively late growth, so that there has been less time for the storing up, by saving, of the necessary machinery.

So it comes about that new countries are in greater need of capital than old ones and consequently are ready to pay a higher rate of interest for it to lenders or to tempt shareholders with a higher rate of profit. And so the opportunity is given to investors in England to develop the agricultural or industrial resources of all the countries under the sun to their own profit and to that of the countries that it supplies. When, for example, the Government of one of the Australian colonies came to London to borrow money for a railway, it said in effect to English investors, "Your railways at home have covered your country with such a network that there are no more profitable lines to be built. The return that you get from investing in them is not too attractive in view of all the trade risks to which they are subject. Do not put your money into them, but lend it to us. We will take it and build a railway in a country which wants them, and, whether the railway pays or no, you will be creditors of a Colonial Government with the whole wealth of the colony pledged to pay you interest and pay back your money when the loan falls due for repayment." For in Australia the railways have all been built by the Colonial Governments, partly because they wished, by pledging their collective credit, to get the money as cheaply as possible, and keep the profits from them in their own hands, and partly probably because they did not wish the management of their railways to be in the hands of London boards. In Argentina, on the other hand, the chief railways have been built, not by the Government but by English companies, shareholders in which have taken all the risks of the enterprise, and have thereby secured handsome profits to themselves, tempered with periods of bad traffic and poor returns.

For many years there was a good deal of prejudice in England against investing abroad, especially among the more sleepy classes of investors who had made their money in home trade, and liked to keep it there when they invested it. As traders, we learnt a world-wide outlook many centuries before we did so as investors. To send a ship with a cargo of English goods to a far off country to be exchanged into its products was a risk that our enterprising forefathers took readily. The ship took in its return cargo and came home, bringing its sheaves with it in a reasonable time, though the Antonios of the period sometimes had awkward moments if their ships were delayed by bad weather, and they were liable on a bond to Shylock. But it was quite another matter to lend money in a distant country when communication was slow and difficult, and social and political conditions had not gained the stability that is needed before contracts can be entered into extending over many years. International moneylending took place, of course, in the middle ages, and everybody knows Motley's great description of the consternation that shook Europe when Philip the Second repudiated his debts "to put an end to such financiering and unhallowed practices with bills of exchange."[3] But though there were moneylenders in those days who obliged foreign potentates with loans, the business was in the hands of expert professional specialists, and there was no medieval counterpart of the country doctor whom we have imagined to be developing industry all over the world by placing his savings in foreign countries. There could be no investing public until there were large classes that had accumulated wealth by saving, and until the discovery of the principle of limited liability enabled adventurers to put their savings into industry without running the risk of losing not only what they put in, but all else that they possessed. By means of this system, the risk of a shareholder in a company is limited to a definite amount, usually the amount that has been paid up on his shares or stock, though in some cases, such as bank and insurance shares, there is a further reserve liability which is left for the protection of the companies' customers.

In the eighteenth century a great outburst of gambling in the East Indian and South Sea companies, and a horde of less notorious concerns was a short-lived episode which must have helped for a very long time to strengthen the natural prejudice that investors feel in favour of putting their money into enterprise at home; and it was still further strengthened by the disastrous results of another great plague of bad foreign securities that smote London just after the war that ended at Waterloo. This prejudice survived up to within living memory, and I have heard myself old-fashioned stockbrokers maintain that, after all, there was no investment like Home Rails, because investors could always go and look at their property, which could not run away. Gradually, however, the habit of foreign investment grew, under the influence of the higher rates of interest and profit offered by new countries, the greater political stability that was developed in them, and political apprehensions at home. In fact it grew so fast and so lustily that there came a time, not many years ago, when investments at home were under a cloud, and many clients, when asking their brokers where and how to place their savings, stipulated that they must be put somewhere abroad.

This was at a time when Mr. Lloyd George's financial measures were arousing resentment and fear among the investing classes, and when preachers of the Tariff Reform creed were laying so much stress on our "dying industries" that they were frightening those who trusted them into the belief that the sun was setting on our industrial greatness. The effect of this belief was to bring down the prices of home securities, and to raise those of other countries, as investors changed from the former into the latter.

So the theory that we were industrially and financially doomed got another argument from its own effects, and its missionaries were able to point to the fall in Consols and the relative steadiness of foreign and colonial securities which their own preaching had brought about, as fresh evidence of its truth. At the same time fear of Socialistic legislation at home had the humorous result of making British investors fear to touch Consols, but rush eagerly to buy the securities of Colonial Governments which had gone much further in the direction of Socialism than we had. Those were great days for all who handled the machinery of oversea investment and in the last few years before the war it is estimated that England was placing some 200 millions a year in her colonies and dependencies and in foreign countries. Old-fashioned folk who still believed in the industrial strength and financial stability of their native land waited for the reaction which was bound to follow when some of the countries into which we poured capital so freely, began to find a difficulty in paying the interest; and just before the war this reaction began to happen, in consequence of the default in Mexico and the financial embarrassments of Brazil. Mexico had shown that the political stability which investors had believed it to have achieved was a very thin veneer and a series of revolutions had plunged that hapless land into anarchy. Brazil was suffering from a heavy fall in the price of one of her chief staple products, rubber, owing to the competition of plantations in Ceylon, Straits Settlements and elsewhere, and was finding difficulty in meeting the interest on the big load of debt that the free facilities given by English and French investors had encouraged her to pile up. She had promised retrenchment at home, and another big loan was being hatched to tide her over her difficulties—or perhaps increase them—when the war cloud began to gather and she has had to resort for the second time in her history to the indignity of a funding scheme. By this "new way of paying old debts" she does not pay interest to her bondholders in cash, but gives them promises to pay instead, and so increases the burden of her debt, which she hopes some day to be able to shoulder again, by resuming payments in cash.

Mexico and Brazil were not the only countries that were showing signs, in 1914, of having indulged too freely in the opportunities given them by the eagerness of English and French investors to place money abroad. It looked as if in many parts of the earth a time of financial disillusionment was dawning, the probable result of which would have been a strong reaction in favour of investment at home. Then came the war with a short sharp spell of financial chaos followed by a halcyon period for young countries, which enabled them to sell their products at greatly increased prices to the warring powers and so to meet their debt charges with an ease that they had never dreamt of, and even to find themselves lending, out of the abundance of their war profits, money to their creditors. America has led the way with a loan of £100 millions to France and England, and Canada has placed 10 millions of credit at the disposal of the Mother Country. There can be little doubt that if the war goes on, and the neutral countries continue to pile up profits by selling food and war materials to the belligerents, many of them will find it convenient to lend some of their gains to their customers. America has also been taking the place of France and England as international moneylenders by financing Argentina; and a great company has been formed in New York to promote international activity, on the part of Americans, in foreign countries. "And thus the whirligig of time," assisted by the eclipse of civilization in Europe, "brings in his revenges" and turns debtors into creditors. In the meantime it need hardly be said that investment at home has become for the time being a matter of patriotic duty for every Englishman, since the financing of the war has the first and last claim on his savings.

Our present concern, however, is not with the war problems of to-day, but with the processes of international finance in the past, and perhaps, before we get to the end, with some attempt to hazard a glimpse into its arrangements in the future. What was the effect on England, and on the countries to whom she lent, of her moneylending activity in the past? As soon as we begin to look into this question we see once more how close is the connection between finance and trade, and that finance is powerless unless it is supported and in fact made possible by industrial or commercial activity behind it. England's international trade made her international finance possible and necessary. A country can only lend money to others if it has goods and services to supply, for in fact it lends not money but goods and services.

In the beginnings of international trade the older countries exchange their products for the raw materials and food produced by the new ones. Then, as emigrants from the old countries go out into the new ones, they want to be supplied with the comforts and appliances of the older civilizations, such as, to take an obvious example, railways. But as the productions of the new countries, at their early stage of development, do not suffice to pay for all the material and machinery needed for building railways, they borrow, in effect, these materials, in the expectation that the railways will open out their resources, enable them to put more land under the plough and bring more stuff to the seaboard, to be exchanged for the products of Europe. The new country, New Zealand or Japan, or whichever it may be, raises a loan in England for the purpose of building a railway, but it does not take the money raised by the loan in the form of money, but in the form of goods needed for the railway, and sometimes in the form of the services of those who plan and build it. It does not follow that all the stuff and services needed for the enterprise are necessarily bought in the country that lends the money; for instance, if Japan borrows money from us for a railway, she may buy some of the steel rails and locomotives in Belgium, and instruct us to pay Belgium for her purchases. If so, instead of sending goods to Japan we shall have to send goods or services to Belgium, or pay Belgium with the claim on some other country that we have established by sending goods or services to it. But, however long the chain may be, the practical fact is that when we lend money we lend somebody the right to claim goods or services from us, whether they are taken from us by the borrower, or by somebody to whom the borrower gives a claim on us.

If, whenever we made a loan, we had to send the money to the borrower in the form of gold, our gold store would soon be used up, and we should have to leave off lending. In other words, our financiers would have to retire from business very quickly if it were not that our manufacturers and shipowners and all the rest of our industrial army produced the goods and services to meet the claims on our industry given, or rather lent, to other countries by the machinery of finance.

This obvious truism is often forgotten by those who look on finance as an independent influence that can make money power out of nothing; and those who forget it are very likely to find themselves entangled in a maze of error. We can make the matter a little clearer if we go back to the original saver, whose money, or claims on industry, is handled by the professional financier. Those who save do so by going without things. Instead of spending their earnings on immediate enjoyment they spend part of them in providing somebody else with goods that they need, and taking from that somebody else an annual payment for the use of these goods for a certain period, after which, if it is a case of a loan, the transaction is closed by repayment of the advance, which again is effected by a transfer of goods. When our country doctor subscribes to an Australian loan raised by a colony for building a railway, he hands over to the colony money which a less thrifty citizen would have spent on pleasures and amusements, and the colony uses it to buy railway material. Thus in effect the doctor is spending his money in making a railway in Australia. He is induced to do so by the promise of the colony to give him £4 every year for each £100 that he lends. If there were not enough people like him to put money into industry instead of spending it on themselves, there could be no railway building or any other form of industrial growth. It is often contended that a reconstruction of society on a Socialistic basis would abolish the capitalist; but in fact it would make everybody a capitalist because the State would have to make the citizens as a whole go without certain immediate enjoyments and work on the production of the machinery of industry. Instead of saving being left to the individual and rewarded by a rate of interest, it would be imposed on all and rewarded by a greater productive power, and consequent increase in commodities, enjoyed by the community and distributed among all its members. The advantages, on paper, of such an arrangement over the present system are obvious. Whether they would be equally obvious in practice would depend on the discretion with which the Government handled the enormous responsibility placed in its hands. But the essential fact that capital can only be got by being saved, and earns the reward that it gets, would remain as strongly in force as ever, and will do so until we have learnt to make goods out of nothing and without effort.

Going back to our doctor, who lends railway material to an Australian colony, we see that every year for each £100 lent the colony has to send him £4. This it can only do if its mines and fields and factories can turn out metals or wheat or wool, or other goods which can be shipped to England or elsewhere and be sold, so that the doctor's £4 is provided. And so though on both sides the transaction is expressed in money it is in fact carried out in goods, both when the loan is made and the interest is paid. And finally when the loan is paid back again, the colony must have sold goods to provide repayment, unless it meets its debts by raising another. But when a loan is well spent on a railway that is needed for the development of a fertile or productive district, it justifies itself by cheapening transport and quickening the output of wealth in such a manner, that the increased volume of goods that it has helped to create easily meets the interest due to lenders, provides a fund for its redemption at maturity, and leaves the borrower better off, with a more fully equipped productive system.

Since, then, there is this close and obvious connection between finance and trade, it is inevitable that all who partake in the activities of international finance should find their trade quickened by it. England has lent money abroad because she is a great producer, and certain classes of Englishmen are savers, so that there was a balance of goods available for export, to be lent to other countries. In the early years of the nineteenth century, when our industrial power was first beginning to gather strength, we used regularly to export goods to a greater value than we imported. These were the goods that we were lending abroad, clearly showing themselves in our trade ledger. Since then the account has been complicated by the growth of the amount that our debtors owe us every year for interest, and by the huge earnings of our merchant navy, which other countries pay by shipping goods to us, so that, by the growth of these items, the trade balance sheet has been turned in the other direction, and in spite of our lending larger and larger amounts all over the world we now have a balance of goods coming in. Interest due to us and shipping freights and the commissions earned by our bankers and insurance companies were estimated before the war to amount to something like 350 millions a year, so that we were able to lend other countries some 200 millions or more in a year and still take from them a very large balance in goods. After the war this comfortable state of affairs will have been modified by the sales that we are making now in New York of the American Railroad bonds and shares that represented the savings that we had put into America in former years, and by the extent of our war borrowings in America, and elsewhere, if we widen the circle of our creditors. The effect of this will be that we shall owe America for interest on the money that it is lending us, and that it will owe us less interest, owing to the blocks of its securities that it is buying back. Against this we shall be able to set debts due to us from our Allies, but if our borrowings and sales of securities exceed our lendings as the war goes on, we shall thereby be poorer. Our power as a creditor country will be less, until by hard work and strict saving we have restored it. This we can very quickly do, if we remember and apply the lessons that war is teaching us about the number of people able to work, whose capacity was hitherto left fallow, that this country contained, and also about the ease with which we can dispense, when a great crisis makes us sensible, with many of the absurdities and futilities on which much of our money, and productive capacity, used to be wasted.

FOOTNOTES: